Concerns about the going concern assumption during an audit

May 20, 2021

After peaking in fiscal year 2008, the estimated total of going concerns for fiscal year 2019 fell to the lowest amount in 20 years, according to a recent study by Audit Analytics. Unfortunately, the COVID-19 pandemic caused financial distress that could bring an end to this downward trend for fiscal year 2020.

A fundamental assumption

The going concern assumption underlies all financial reporting under U.S. Generally Accepted Accounting Principles (GAAP). It presumes that a company will continue normal business operations into the future. When liquidation is imminent, the liquidation basis of accounting is used instead.

The final responsibilities to decide whether there’s a going concern issue and provide related footnote disclosures shifted from external auditors to the company’s management, under Accounting Standards Update (ASU) No. 2014-15, Presentation of Financial Statements — Going Concern (Subtopic 205-40): Disclosure of Uncertainties About an Entity’s Ability to Continue as a Going Concern. Essentially, the going concern accounting standard requires management to decide whether there are conditions or events that raise substantial doubt about the company’s ability to continue as a going concern within one year after the date that the financial statements are issued (or within one year after the date that the financial statements are available to be issued, to prevent auditors from holding financial statements for several months after year end to see if the company survives).

Substantial doubt exists when relevant conditions and events, considered in the aggregate, indicate that it’s probable that the company won’t be able to meet its current obligations as they become due. Examples of adverse conditions or events that might cause management to doubt the going concern assumption include:

- Recurring operating losses,

- Working capital deficiencies,

- Loan defaults,

- Asset disposals, and

- Loss of a key franchise, customer or supplier.

Financial distress experienced during the pandemic could cause these types of adverse conditions or events, potentially leading to an uptick in going concern issues for the 2020 fiscal year — and possibly beyond.

After management identifies that a going concern issue exists, it should consider whether any mitigating plans will alleviate the substantial doubt. Examples of corrective actions include plans to raise equity, borrow money, restructure debt, cut costs or dispose of an asset or business line.

A consistent approach

The Auditing Standards Board’s Statement on Auditing Standards (SAS) No. 132, The Auditor’s Consideration of an Entity’s Ability to Continue as a Going Concern, is intended to promote consistency between the auditing standards and accounting guidance under U.S. GAAP. The current auditing standard requires auditors to obtain sufficient appropriate audit evidence regarding management’s use of the going concern basis of accounting in the preparation of the financial statements. The standard also calls for auditors to conclude on the appropriateness of management’s assessment.

The evaluation of whether there’s substantial doubt about a company’s ability to continue as a going concern can be performed only on a complete set of financial statements at an enterprise level. So, the going concern auditing standard doesn’t apply to audits of single financial statements, such as balance sheets and specific elements, accounts, or items of a financial statement.

Auditors as gatekeepers

Management is responsible for making the going concern assessment. They must provide appropriate documentation to prove to external auditors that management’s assessment is reasonable and complete. Due to market volatility during the pandemic, your auditors are likely to scrutinize this assessment even more closely in upcoming audits.

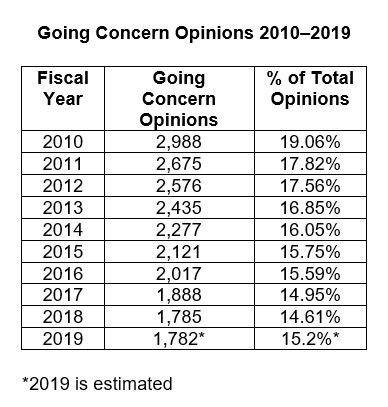

Going Concern: Audit Opinion Trends

Audit Analytics reviewed the population of audit opinions filed with the Securities and Exchange Commission (SEC) as of November 13, 2020, to determine the number of opinions qualified by an uncertainty regarding the going concern assumption. This analysis reported the following statistics about going concern audit opinions issued over the last decade:

This table shows that the number of going concern opinions fell by about 40% from 2,988 in 2010 to 1,782 in 2019. Audit Analytics doesn’t attribute the decrease in the number of going concern opinions for 2019 to improved company performance. Rather, it’s linked to “attrition from the prior year’s going concern population.” In other words, many of the companies that filed a going concern opinion for 2018 “disappeared.” That could mean the company filed a termination of registration, had its registration revoked, went private, closed, liquidated or simply didn’t file an audit opinion for 2019.

In addition, a small number of companies that filed a going concern opinion for 2018 subsequently “improved.” In other words, these companies filed a clean audit opinion for 2019, because there was no longer substantial doubt over its ability to continue as a going concern.

Audit Analytics also tracks the reasons that auditors give for their apprehension over a company’s going concern status. The top five issues listed for fiscal year 2019 are:

Going Concern: Audit Opinion Trends

Audit Analytics reviewed the population of audit opinions filed with the Securities and Exchange Commission (SEC) as of November 13, 2020, to determine the number of opinions qualified by an uncertainty regarding the going concern assumption. This analysis reported the following statistics about going concern audit opinions issued over the last decade:

This table shows that the number of going concern opinions fell by about 40% from 2,988 in 2010 to 1,782 in 2019. Audit Analytics doesn’t attribute the decrease in the number of going concern opinions for 2019 to improved company performance. Rather, it’s linked to “attrition from the prior year’s going concern population.” In other words, many of the companies that filed a going concern opinion for 2018 “disappeared.” That could mean the company filed a termination of registration, had its registration revoked, went private, closed, liquidated or simply didn’t file an audit opinion for 2019.

In addition, a small number of companies that filed a going concern opinion for 2018 subsequently “improved.” In other words, these companies filed a clean audit opinion for 2019, because there was no longer substantial doubt over its ability to continue as a going concern.

Audit Analytics also tracks the reasons that auditors give for their apprehension over a company’s going concern status. The top five issues listed for fiscal year 2019 are:

- Net or operating losses (including recurring losses),

- Working capital or current ratio deficit,

- Negative cash flows from operations,

- Accumulated or retained earnings deficit, and

- Insufficient or limited cash, capital or liquidity concerns.

© 2021